Inverted Yield Curve = Recession

When the yield of the ten-year Treasury note is less than the yield of the two-year Treasury note (inverted yield curve), a recession has followed in the next 12 to 24 months for the last three decades. So it is worthy of note that recently the yield of the two-year Treasury note and the yield of the three-year Treasury note were higher than the yield of the five-year Treasury note.

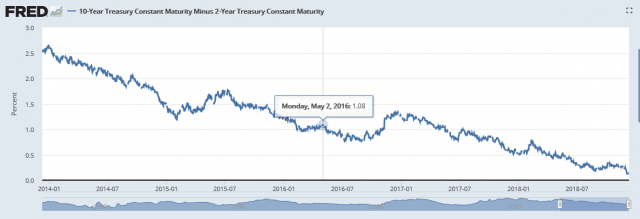

The Fed chart above tracks the difference in yield between the 10-year note and the 2-year note. One can see that it is “flattening” as of 11 December 2018. That means that the spread, the difference, is becoming smaller and smaller. That is, the yield of the 10-year note has become only a bit more than the yield of the 2-year note.

What this means for investors is that there is demand for the 10-year notes even though the Fed has been raising interest rates, which means that shorter term notes provide a higher yield than before. Given that the Fed has been reducing its balance by $60 billion a month while at the same time raising interest rates, this means that credit conditions are tightening. This means that companies will have difficulty in finding financing and will have to pay more to service their debts when they do find financing.

This is extremely bad news for the American fracking Ponzi scheme companies that have been producing negative cash flow for years and are heavily indebted. It is also bad news for the shareholders of these companies since higher costs for servicing debt may force some of these companies into bankruptcy. It goes without saying that the US federal government is going to have some problems servicing its debt, which is now $21.8 trillion. Inflation is probably how the US government is going to solve its debt problem.

Walter Snyder

info@swissfinancialconsulting.ch

Disclaimer

This Newsletter has been prepared by WWS Swiss Financial Consulting SA (the company). Even though every effort has been taken to ensure the accuracy of the content of the Newsletter, there is absolutely no guarantee that the information contained in it is correct, up-to-date, accurate or otherwise applicable. It is not intended as a solicitation, invitation or recommendation for the purchase or sale of any investment fund or product or security or financial instrument or to participate in any particular trading strategy or banking product in any jurisdiction. It is not to be distributed in any country or area where it is legally prohibited. No liability whatsoever is or will be assumed by the company for any damage, loss or negative result of any sort ensuing from following views expressed and contained in the Newsletter. Investors themselves assume the full risk for any decisions that they take (caveat emptor). The Newsletter may not be reproduced or published by anyone anywhere in any way or form without the express written permission of the company.