Behavioural Finance: Human, all too human

Empirical evidence thus shows that the efficient market hypothesis can at best be understood in normative terms but its basic grounding in reality is by no means assured. This is where behavioural finance comes in. Behavioural finance focuses on the decisions of individual persons and the aggregated impact of irrational thinking and behaviour on the market level. There are many traps here, and investors are not the only ones to be ensnared by them:

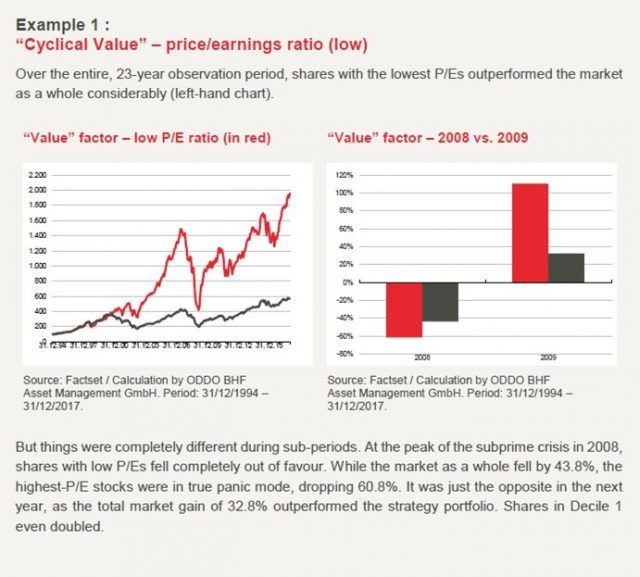

CASE STUDY:

Test subjects were given the following choice in a study:

A. You have 50% change of winning EUR 1000

B. You have a 100% chance of winning EUR 500

Statistically speaking, both answers are equivalent, and yet the overwhelming majority of respondents chose the safe EUR 500 gain.

Another test group was given the following choice:

A. You have 50% change of losing EUR 1000

B. You have a 100% chance of losing EUR 500

This time the overwhelming majority opted for the riskier choice “A”.

This case study is based on the so-called disposition effect, i.e., investors’ tendency to realise gains too early and to hold on to losing positions too long. This behaviour affects investment success, as it contradicts the observable tendency of stocks that have recently risen in value to keep doing well. So, fear of losing is enough to make one assume a greater risk, whereas when there is a possibility of a gain, one is more satisfied with a moderate outcome. This study shows that the risk of loss has a higher emotional value in decision-making situations than potential gains.

A related phenomenon is “anchoring”. Share prices at any one time often reflect less the firm’s current earnings situation. Rather, there are other factors more strongly at play, such as historical highs, cost basis, or, in some cases, round numbers such as 100 or 1000. Chart analysis arose as an investment strategy based on this behavioural pattern. It is not rational to continue to be guided by a five- or 10-year-old high. The company in question may be far more profitable now or it may have realigned its strategy. Chartists compare only the price of a share while ignoring the company’s degree of success. This has implications for capital markets, as investors follow herd instincts that drive them to invest in assets that many other investors are investing in. So, the more people keep an eye on the same milestones, the greater the probability that they buy stocks until these milestones have been reached, hence creating a self-fulfilling prophecy.

Other widespread irrational behaviours in the investment world include calculated optimism and the herd mentality. However, there are many more of these, as our illustration shows.

What about market behaviour? Since science has shown that people make poor decisions when relying on their emotions, the question begs itself: “Why indeed do we decide in the heat of the moment?” When shares that we consider cheap are driven down in value by irrational emotions, their undervaluation objectively looks even greater. Markets can be irrational for a long time, but not forever. As Joel Greenblatt said:

“Over the short term, Mr. Market acts like a wildly emotional guy who can buy or sell stocks at depressed or inflated prices. Over the long run, it’s a completely different story. Mr. Market gets it right.”

(Joel Greenblatt, « The Little Book that beats the Market », 2010)

On a long-term view, it is worth investing independently of market mood. Not letting yourself be infected with market panic and, instead, resisting all temptation and sticking to your convictions is easier said than done. Just as Odysseus had himself tied to the mast of his ship to keep himself from giving in to the seductive song of the sirens, investors must protect themselves from their emotions if they are to achieve success.

Dr. Carsten Große-Knetter

Global Head of Quantitative Equity, ODDO BHF Asset Management

Thierry Misamer

Portfolio Manager, ODDO BHF Asset Management