The US rate hike

Possible misfire from the side of the Fed?

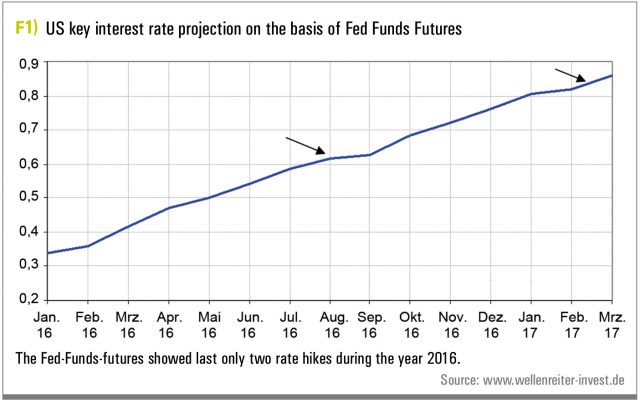

In 2015, 75 interest rate cuts have been performed worldwide, five of them in China. By contrast, there were 51 interest rate hikes, the last of them enjoyed the highest media attention: On 12/16/2015, the US Federal Reserve (Fed) had the courage to end the since 2008 ongoing zero interest rate policy. The increase in the US key interest rate from 0.12 to 0.37 percent in December 2015 was a small step- the sign of the end of an era could be a big step. However, this assumes that the Fed may actually initiate an interest increase cycle. The projection of the Fed for the further development of the US prime rate suggests an average interest rate of 1.38 percent at the end of the year 2016th. At the end of 2017, is 2,38 percent forecast, end of 2018 the interest rate should have a value of 3.25 percent. This contradicts the Fed Funds futures, which reflects investors’ expectations. They only show two rate hikes during the year 2016 (Figure 1).

A further increase of the effective Fed-Funds-rate is priced only for the summer 2016 at 100 percent (an increase of 25 basis points from 0.37 to 0.62 percent). A second rate hike – then to 0.87 percent – is expected only in early 2017th. Even by the monthly fund-manager-survey by Bank of America / Merrill Lynch almost two thirds of investors expect only two or three rate hikes in 2016th. The investors do not believe in the projections of the Fed carried out in the December 2015 survey.

Does it come differently?

Surprises for investors could be first in a stronger rate hike path or second in a quasi-non-happening interest increase cycle – after a step would stop. Considering the evolution of commodity prices, the skepticism of the investors is more than understandable. In the first half of 2016, the economic momentum is likely to continue to decline at least until April 2016th. In this respect, a first rate hike in 2016 before the summer seems really unlikely. It would depend on the dynamics of economic decline. Since the basic effects of inflation by a turnaround in commodity prices, lead to a rise of the inflation over its core rate, the second interest increase could be expected only in December 2016 – after the US-election. In the run-up to US presidential election the Fed is normally holding back, so that no rate hikes are to be expected in September and December.

Impact on bonds and equities

We want to show below, the impacts of the start of an interest increase cycle on individual asset classes. Then it is important to scrutinize whether a cycle is initiated.

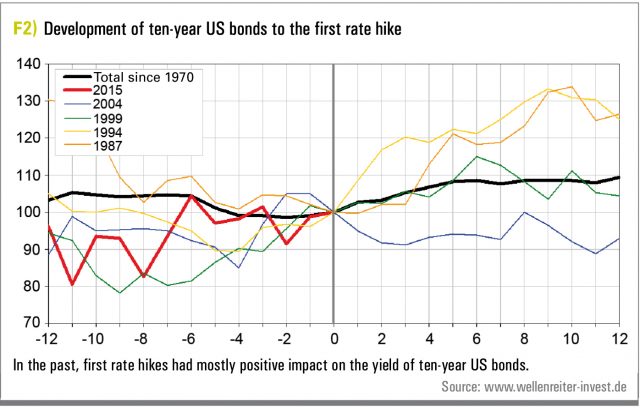

In the past, first rate hikes affected mostly positive the yield of the ten-year US Bonds (Figure 2). However, the influence of the long End through the short End, did not work in 1982 (recession) or in 2004 (Greenspan’s “Conundrum”).The last successful influence dates back to the year 1999. In 1994, a crash occurred in the bond market, and the yield increased significantly. The assumption that an increase in the interest rate leads to increasing yields at the long End, is a miscalculation, even if the average shows rising yields. In 2015, a moderate rise in yields took prior before the first step. The very high net short positions by speculators at five year maturities confirms our skepticism about the effect (vigorous, penetrating -effect) of a rate hike on the middle and long End. These positioning points indicate to rising prices and thus falling yields.

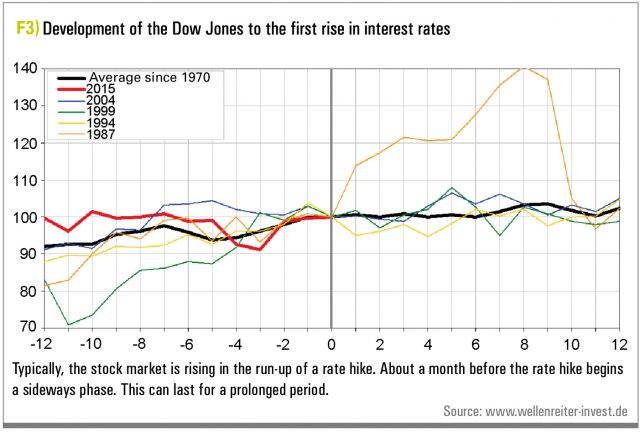

How does the US-stock market react in such a situation? Usually the market is rising in the run-up of a rate hike. About a month before the rate hike begins a sideways phase. This can last for a prolonged period (Figure 3).

The unique exception is the 1987 with its boom-bust cycle. In 2004, the sideways trend of the Dow Jones Index began half a year before the rate hike. This situation in December 2015 was different to cycles since 1987, while the first rate hike took place although the industry shares declined slightly in the past nine months.

Such a development could be observed in the 1976th. If we exclude deliberately the crash of 1987, so was the most negative reaction, after the first interest increase, in December 1976. In 1983 and 1994, the losses were marginal, and in the other cases the US-stock market was quoted after a year at a higher level. In the last three cycles (1994, 1999, 2004), the stock market had in all cases moderate losses after three months. Losses in the first three months are therefore more the rule than the exception.

Does a new cycle begin?

Now that we have shown how the individual markets develop after the start of a normal cycle, we want to think in the next step, whether such a cycle has really begun.

<< The rate hike raised an obstacle for the new QE program in the US. Because, the FED should admit to having made a mistake >>

Japan’s attempts to get out of the zero interest rate policy have failed twice in the 2000s. Japan increased the interest rates twice in July 2006 and February 2007 and was by that decision too late in the global cycle, as the US-economy had already gradually approached the financial crisis, by the inverted yield curve. Previously, the attempt with a single rate hike in August 2000 failed. In both cases, there were particular in the US–market clear signs of an economic slowdown which led in the following years to a recession. Therefore, there is a risk that the Fed has acted too late in the cycle.

The first rate hike in December 2015 raised once more obstacles for the new edition of a quantitative easing program (QE) in the US, because the US-Fed should admit that they have made a mistake. The price losses in August 2015 have not been sufficient to move the Fed to further support measures. Greater losses (below the August lows) and a significant economic slowdown (recession or at least fear of recession) accompanied by a worsening in the US labor market, were necessary to cause a rethink in the direction at the Fed.

In the last years, the US-Federal Reserve caused with help of the QE programs reflationary trend movements. This support is not given in the current environment. If the Fed Chairman Janet Yellen on 02.12.2015 using the words “As such, it is a day on which we are, in my opinion, all rejoicing” lies the focus of the US central bank on an interest increase cycle, then such a move cannot be reversed after a period of hesitation. The Fed Vice Stanley Fischer noticed in the first days of 2016 that investors would underestimate the interest increase by the Fed and expect four key rate increases in 2016th. So it is clear, that there will be no support for the investors from the US Federal reserve.

The proverb “Do not fight the Fed” is in the foreground. Ultimately, market forces will prevail over the assessment of the US Federal Reserve. However, Fisher’s quote shows that the pain of the US central banker should increase. The US Federal Reserve, which describes its approach as a “data-dependent”, is therefore likely to maintain initially its course. The idea of four interest hikes is ultimately wishful thinking. Investors react and will show the Fed what they expect. So far, they expect two steps increase in 2016. This approach is likely to erode in the coming weeks. Only when investors through sales on the stock market keeps pressure on the Fed, so that the central bank will be forced to reject (turn away) its increasing path. Then the markets should calm down. Japan sents his regards.

Author

Robert Rethfeld

Robert Rethfeld betreibt den Börsendienst Wellenreiter-Invest. Kernprodukt ist ein handelstäglich erscheinender, Abonnement-basierter Börsenbrief. Rethfeld ist TV-Interviewpartner, Recherchepartner und Gastautor für „Smart Investor”. Er veröffentlicht Kolumnen bei n-tv.de und anderen Börsendiensten und ist Mitglied bei der VTAD.

Feature article by

![]()